“Are you ready?”

She asked me the question. I feel it’s important to share given that so many women do not own homes outright in their own name. This decision was an important one my husband and I made together years ago. We wanted to move beyond years of renting into home ownership and the transition was possible because I purchased the home solely in my name. His student debt had become a challenge to this transition much like I had to overcome unemployment and build a solid two years of consistent employment for banks to even give me a chance.

A few short minutes ago my husband and I finished initialing and signing our future on a new property, one that I would visit after relinquishing my claim to the old home. I had already said goodbye, cleaning the house as best I could. I had some regrets about the aging carpet upstairs that held onto years of pet grim and the unfortunate team that had installed the new carpet downstairs a few weeks prior but overall I was ready. Selling the home would pay off the home loan and we were walking away with a profit.

For once, it seemed like I had the right timing for a financial goal.

After paying the commissions for the real estate agents, our profit exceeded my yearly income. The gamble to ignore some of Dave Ramsey’s financial advice paid off.

This is the time for a disclaimer. I am not sharing my story as financial advice for someone else to follow. I lack the financial certifications to guide someone to make her (or his) financial choices. Instead I am sharing my experiences to demonstrate how a life choice paid off and to inspire others to look critically at financial resources as a combination of tools to succeed.

One of the best ways to have this discussion is to take a step back and talk to you about the last rental we lived in before we took the leap into first time home ownership.

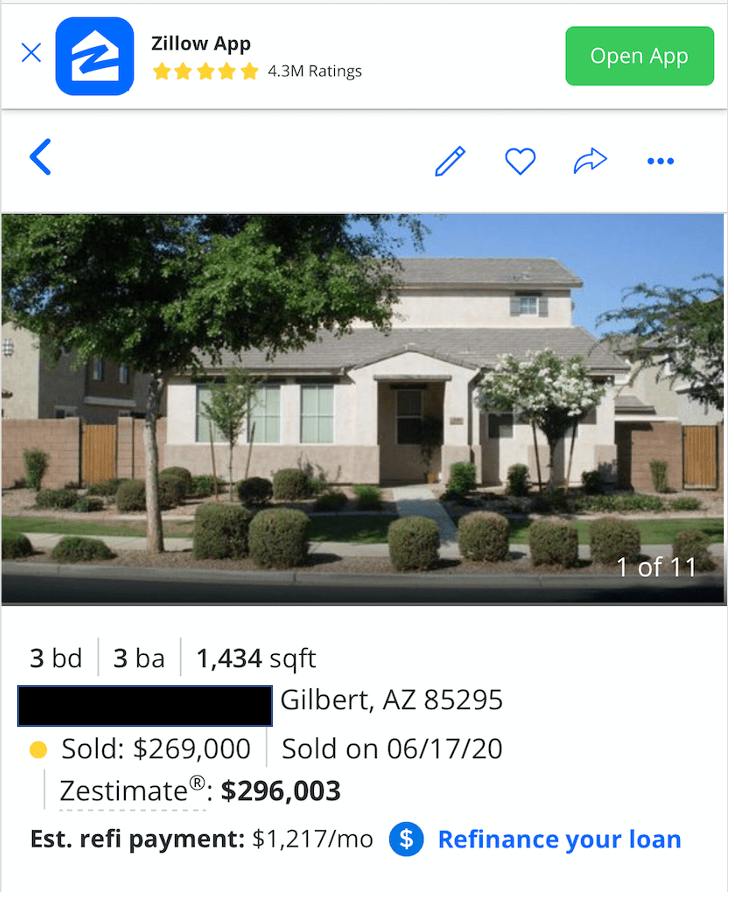

I was still repairing my employment history in 2015 when this home sold for $174,000. I would not have two stable years of employment under my belt again until October of that year so lenders wouldn’t look at me as financially capable for home ownership purposes. The monthly housing allowance I received as a veteran using Chapter 33 Post-9/11 benefits to pay for my graduate degree could not count as income which would have helped. Instead of having the freedom to apply the $1,461 monthly housing allowance to a mortgage, I was using it to pay $1,270.62 to the property management company utilized by the home investor.

Like other renters, we knew our rent price was not stable and home prices were also increasing. I had started looking at homes in Arizona in 2011 and here are some that I previously shared on another blog of mine.

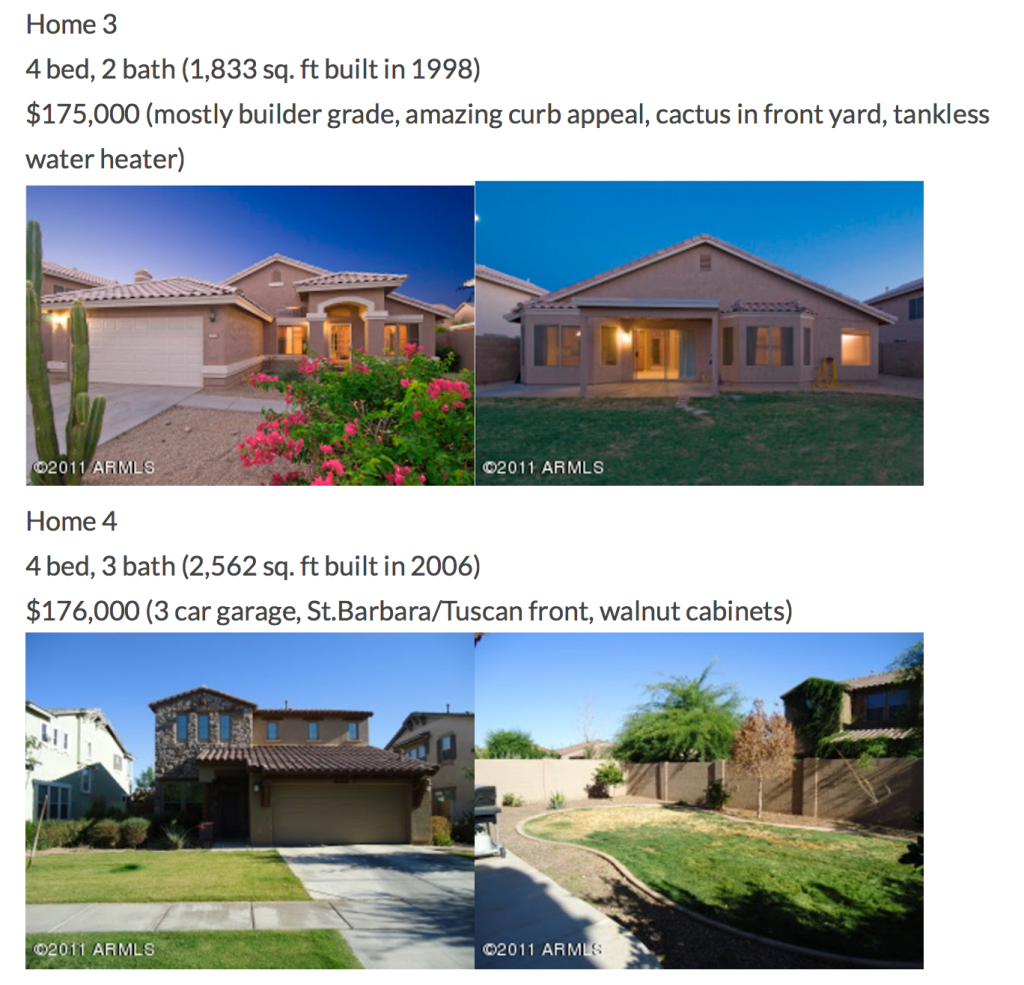

We missed out on some really good contenders September 2011 due to how the housing bubble burst in Arizona such as the following:

We missed the mark in home buying in 2011-2012 due to not properly planning our move to Arizona and also not having a network that clued us in on how to best transition out of the Marine Corps for my husband. Granted, as I say this, I also think how best to transition from college graduate to newly hired employee. Reflecting back on our experiences, it would have been wise as well to cast a wider net than choosing Arizona specifically. When my husband turned away an unappealing offer from the Marine Corps for his next tour of duty, we were stuck in Wyoming a year longer than expected.

The time could have been better utilized. I think my concerns about getting out of debt were really in the way of viewing the situation with fresh eyes. We knew California was unaffordable, as was Rhode Island where my family lives, and we aren’t fans of the cold so Arizona seemed a reasonable place to land. I opted out of pursuing a career with the Naval Criminal Investigative Service, the place I interned, because signing a mobility agreement wasn’t as enticing after the Marine Corps landed us in Wyoming. (Still, I love my friends. I don’t like Wyoming.) When I plotted a different career path, I should have considered other federal agencies that offered me something similar to the enjoyment I felt during my internship in places with as reasonable a cost of living as was available in Arizona around the time of our move in 2012.

Can you tell I am still trying to forgive myself for not being a better planner?

Other things have fallen into place though so I’ll get back on track with today’s conversation.

This home that sold for $174,000, our old rental, was a source of inspiration to get off our butts and start figuring out what financial advice worked (and didn’t work) for our unique circumstances. At the time, it was as close to my budget minded “dream home”. It has a beautiful pie-shaped lot, perhaps the largest in the community, granite counters in the kitchen, and a guest bedroom downstairs. We rented it knowing very well there was probably no chance it would be back on the market for years. Just hazarding a guess here, but if the pandemic had not happened, I think it would still be owned by the investor.

As we came closer to a year in our rental, we began investigating our home opportunities. A handful of options quickly dwindled to almost none. A 1990’s home with a shared driveway in Gilbert’s Western Skies neighborhood fell off our list of potentials as did a townhouse in The Gardens and a one bedroom and a den described quite falsely as a two bedroom home in the Lakes at Annecy community which had a lakefront view. For me, Dave Ramsey’s teachings were the place to start, to understand I needed a budget. I had to tune out his voice and others that stated you should only buy property with cash or if you hold a mortgage it should be a fifteen year mortgage or you should only buy a house when you have no debt or (insert a small debt threshold here). We don’t live in as high a rent cost area as parts of New York City or the San Francisco area, but Gilbert was quickly becoming unaffordable and rising rent costs along with stagnant wages meant revisiting my views on money. I had to learn what others learned much earlier and that is that “Personal finance is personal.” Today, I even listened to a podcaster who stated something to the effect “You are a ‘You’ expert.” as a way to express why we shouldn’t let how others direct their financial wellbeing direct how we budget our money. If you want to listen to her guidance, check out Frugal Debt Free Life. The podcast episode is Episode 16: How to not feel like crap about your money.

To become a first time homeowner, I leveraged a situation that is not replicable to all persons at a time when I did not understand I was the “You” expert in my life. Here’s how it worked out. I used a VA home loan with zero down, trusting in what I saw in the market, our years removed from the 2008 recession. We still had closing costs to contend with, but each homeowner will have some things that will be their responsibility and some things that are the seller’s responsibility. Case in point, when I sold our home last year, the commissions came out of my pocket. Our home expenditure (excluding HOA) dropped from our rental price of $1,270.62 to a mortgage of $903.07. Not all Gilbert neighborhoods have HOA’s, but most do and we paid a separate additional $80 monthly for community maintenance and a handful of events. The scrimping for closing costs and movers was worth it. Knowing we had planned to stay in the area for a handful of years made it worth it to build more breathing room in our budget using our option of home ownership versus renting. Using our prior rental neighborhood for comparison since I cannot use the home as it is not currently on the market, our rent could have skyrocketed up to the $1,750 to $1,960 some 1400 to 1600 square ft. homes are renting for here in January. By comparison, even with some adjustments to our mortgage payment, our last mortgage payment for the first home was only $959.99.

Home ownership does not work well for all persons, so I am not here to preach it works for everyone. For us, over 44 months of mortgage payments put us in the ballpark of $39,735.08 to $42,239.56. I am using a range because I do not want to track all past payments to show where the mortgage payment increased. Even if the investor would have kept our monthly rate the same as our 2017 rate and we stayed in that rental, he would have received $55,907.28 minus the monthly expense for the property management costs over the same 44 time period. Why make that guy rich? Realistically, rent probably increased at least two times over the last few years putting additional money in his pocket plus the bulk of the $95,000 difference from the purchase price and sale last year during the pandemic.

Originally, I wanted to share the earlier parts of my story with the ChooseFi podcast and it was fortuitous I discovered our old rental sold helping to better flesh out my financial story comparing home ownership to renting in America. Last year, I sent in a short video to be part of their “The Real Households of FI.” When I wasn’t selected, I was let down but as the pandemic dragged on, I felt some relief. There was so much baggage from my deployment that made the pandemic more stressful I would have not presented my situation in the best way as a growing experience. I am taking more of a slow FIRE (Financial Independence Retire Early) approach like Michelle Jackson from michelleismoneyhungry but still listening to the ChooseFi hosts, Brad and Jonathan, reminds me people start on so many different levels and my advantages and disadvantages are not as unique as I once thought they were.

In the past few weeks, I’ve felt incredibly compelled to open up about my feelings on home ownership and the rent crisis going on in the United States. As unsteady as some homeowners have it during the pandemic, most are still starting off in a better spot than renters who are paying a higher cost for their accommodations prior to any job loss or reduction which leaves them more vulnerable. My past experience with unemployment after college, resulting in making me ineligible for unemployment compensation, and my second bout of unemployment in 2013 when Arizona was so far behind on unemployment compensation I was unpaid my three months of job searching are contributing factors to why I started to think “No Thank You.” to some of the gazelle intensity behind Dave Ramsey’s teaching and his generalized view on when individuals are best prepared to step into a new identity as homeowner.

Reflecting back, Dave Ramsey had a financial safety net in the form of bankruptcy although he does not call it that, but this choice allowed him to start over. My path to rebuild my financial wellbeing looked different but it was still challenging and humbling. I would not call my choices stupid as he so often calls consumption, to include his own, because there is so much learning that occurs in our lifetime. I did not grow up seeing employment as something precarious for most of my childhood until my dad was medically separated from the Navy. Instead, I saw civilian employment as steady because my mom worked for the same medical professionals our entire time in southern California and I saw the military as a precarious opportunity due to my dad’s experience. I was unaware if family friends lost their jobs and our neighborhood was never flooded with home foreclosures and short sales like what I witnessed in 2008. My parents taught me college would be an avenue to greater success and therefore I tackled that objective for a year before the Marine Corps, a little during, and completed two of my four degrees when life smacked me in the face in 2012.

I was left to burn through our modest savings during my 2012 unemployment before I was worthy of governmental assistance in the form of SNAP. The team also offered to help me with my unemployment problem were surprised when I indicated I didn’t need help with the job search process; I knew how to do that, but all told I applied for 89 jobs from what I can recall. The hunt, I could do; securing the interview and the job offer was where I was struggling. Almost no one was looking at me. (For all that work, I only ever landed three interview prospects and one job offer.) When confronted with my second stint of unemployment, I choose to empty out roughly six months of Arizona State Retirement contributions because my family could not wait for some money to come in when the state would make unemployment available to me and I had not yet rebuilt our emergency fund. I cannot even tell you what the amount of money from my 2013 retirement contributions would look like today if I had the ability back then to file for unemployment to stay afloat than to take out my money and pay a penalty tax on it.

SNAP was the springboard to reduce some burdens in my family life, but ultimately it took using my veteran benefits to return my family back to middle class. I started with my small portion of Chapter 30 Montgomery GI Bill, something like 13 days, which include the equivalent remaining portion of the Marine Corps College Fund and additional money by paying into the Buy-Up program. Exhausting my CH 30 benefits opened the door to use the 12 months of Post-9/11 GI Bill available to me for which I was rated at 100%. The housing allowance attached to this benefit is something I’ve discussed at length in the past so I won’t go into those details again. Just run a search for Chapter 33 and you’ll find I’m pretty transparent about the financial breakdown. This second step, being paid to attend school, helped further provide breathing room in my budget and that security along with hitting the right window of more recent employment history opened the most recent door to success: home ownership.

With all my struggles, it has been painful to watch our nation’s politicians bicker throughout 2020 and dole out $600 most recently to individuals as part of the stimulus package to provide relief as we continue to cope with the pandemic. I know for many people $600 is less than their monthly rent/mortgage or childcare costs, a topic I hope to speak on a bit more soon. Likely, it is also barely enough for a month’s worth of groceries depending on how many mouths you’re feeding and if anyone has food allergies, certain allergen free goods are more expensive, not allowing those families to extend their grocery dollars as far as others. As I’ve seen our different levels of government struggle to get our nation as safely as possible through the pandemic, I have become more convinced we did the right thing by ignoring many of Dave Ramsey’s teachings. I am not entirely confident if we had needed financial support it would have been made available to us given the high demand we’ve seen this past year and listening to my past was more important than listening to someone who accessed different tools in his time of need.

By flattening his concept of Baby Steps and consolidating Step 1 ($1,000 emergency fund) and Step 3 (the fully funded emergency fund) as our first priority for 2020 after the home sale, we put ourselves into a better situation when the pandemic started to affect our lives in March last year. Groceries started to become more expensive. For a little while, I picked up what I could just because I did not know when the shelves would be stocked again and that often meant picking up more expensive brands because bulk items were no longer available.

I also have no guilt about not tackling our debt with gazelle like intensity. Seriously, when the world feels like it’s failing apart and any one of us is a higher risk of dying, do I really want my family to remember me as ferociously attacking debt my last year of life? No. I maintained progress on certain debts and instead of using the debt snowball as we do look to reduce debt in our lives, I am comfortable taking the debt avalanche approach instead. Goodbye Baby Step 2. With the pause on student loan debt, I used the space in my budget at times to extend aid to friends in need who experienced a death in their family, an unexpected loss of housing, three family members coming down with COVID at the same time, and also increased how much I tipped for service at my favorite restaurants who were dealt a hard blow by the pandemic capacity restrictions placed on them.

I won’t go down the list through the remaining steps but they all lead to Step 7: Build Wealth and Give.

Selling my former home last year was a vital step in wealth building, but it is not a tool everyone needs to succeed. There are so many ways to diversify one’s income sources and I am happy to share how this avenue worked out for me. The other part of my success is affording the same opportunity to others. I can lift up my community in different ways than governmental support can. Using my experiences and understanding the difficult road to home ownership, I took it upon myself to think critically about the future owner of my former residence.

A veteran sold her home to me in 2016 and as a veteran, I also selected another veteran in 2020 who intended to occupy the property. In my opinion, I feel our community is overrun with investors. In fact, the woman who sold my first house to me turned down an investor for the same reasons I did. Neither of us wanted the house to fall into an investor’s hands knowing the struggle it took to rebuild our finances after experiencing difficult circumstances. The prospective investor who provided the first offer on our home had no emotional attachment to the property and provided a significantly lower offer. He was offering something in the ballpark of $30,000 less than list price. His incentive to make his offer appealing was a quick closing for us. Instead, I waited. Another scary decision but one I do not regret. I knew someone would love what we tried to do to make the builder grade property better. And he showed up.

This single dad with two kids. He didn’t need to show up with the best offer, but he did.

My old home found its next family and I entered 2020 with more financial security than my family has experienced in years. Like back to 2006-2007, dual income no kids, but even better.

This home sale was a big deal and I am glad I finally found the courage to speak out about what it means to me. It is a financial win I finally feel like I can celebrate.