I am taking an unpopular stance on the recent memorandum regarding discharging federal student debt for permanently and totally disabled veterans, but hear me out. Like a number of other socially and politically motivated moves, there is in this case a lot of talk on the surface that does not get to the nuances of the situation. My view is informed partially by my work in higher education and my experience as a student who has used the Post-9/11 GI Bill at the 100% level and still made the decision at times to take out student loans without choosing to take on the maximum debt available to me.

To start with, there is no such thing as a perfect policy. It does not matter if we have a Republican president or a Democratic president. It does not matter the distribution of party influence throughout the different levels of our government. There is no policy that can serve the needs of people perfectly because there are rules in place to ensure a standard process for efficiency and ideally, to prevent abuse. Additionally, some people will be served at the expense of others who are excluded from the benefit. That’s just how it goes.

Before I proceed further, you can read the memorandum here.

I want to be transparent our society has not always given great deference to our nation’s veterans. Vietnam veterans know this all too well. There will be some merit to updating the student loan forgiveness policy currently in place, but I do not buy into this effort as something to honor our veterans.

Our society often offers incentives to veterans as a means to cure its own problems.

The incentives are then wrapped in language to appear that veterans are the primary recipients but there are a diverse amount of groups that are also served when veterans (and/or their families) receive benefits. The people who support such measures can help encourage their likelihood of being re-elected. Organizations can use forms of collaboration to cut costs. Different groups can use such measures to be viewed as more “veteran friendly” in comparison to similar public or private competitors. Even the history of VA education benefits started with a mission to help address the reality of unemployed veterans. Since our society has always had something to gain from the “feel good” nature of veteran programs and services, namely the economic output of veterans like other consumers, we should look critically at what is accomplished and also what we don’t intend to happen, but could happen with policy implementation.

Again, I want to reiterate there will be those in need who are properly served by updates to the Total and Permanent Disability Discharge, but the situation is ripe for possible abuse and must also be viewed in light of VA benefits to defray the cost of education.

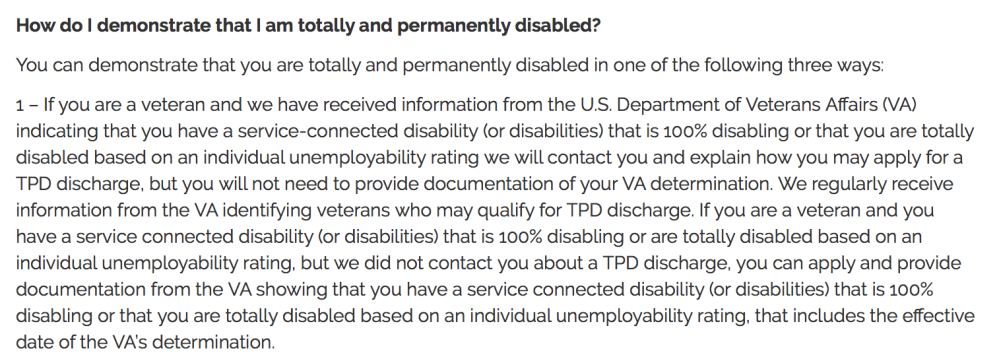

This information from the Federal Student Aid’s website indicates eligible veterans have disabilities that are “100% disabling or that [veterans] are totally disabled based on an individual unemployability rating, that includes the effective date of the VA’s determination.”

A veteran can be 100% disabled for VA purposes but that does not mean he or she is unemployable, which is a significant quality I think this memorandum misses entirely.

It is not necessarily fair to provide the same benefit of student loan forgiveness to a veteran with a 100% disability rating that is employable when there are those 100% totally and permanently disabled veterans for whom work is not possible.

It is this distinction that irks me. And I’ll express my views a bit more to explain why this issue is something I think was grossly overlooked and may have been back when disabled veterans were included as an eligible group. (Perhaps, the website will be updated with more clear language but I think the 100% disabled veteran and the 100% totally and permanently disabled veteran will be treated the same moving forward as well.)

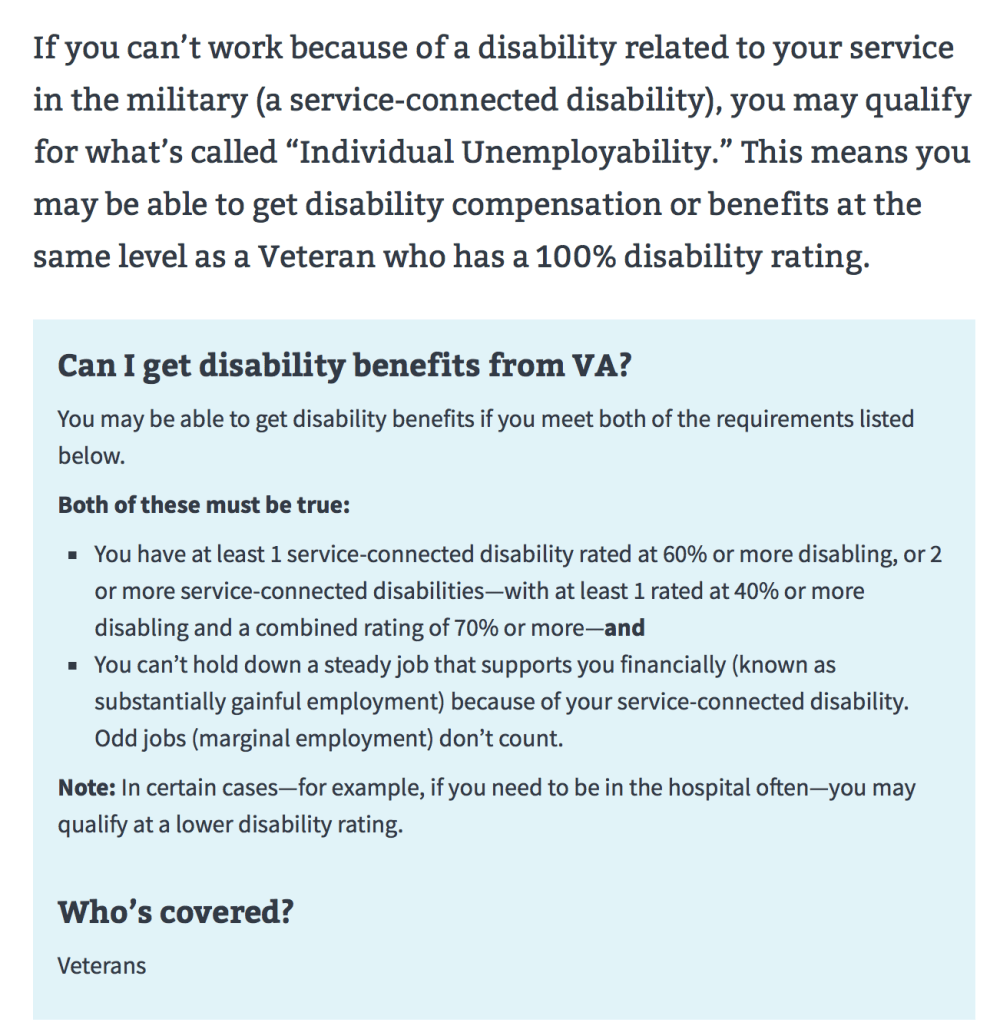

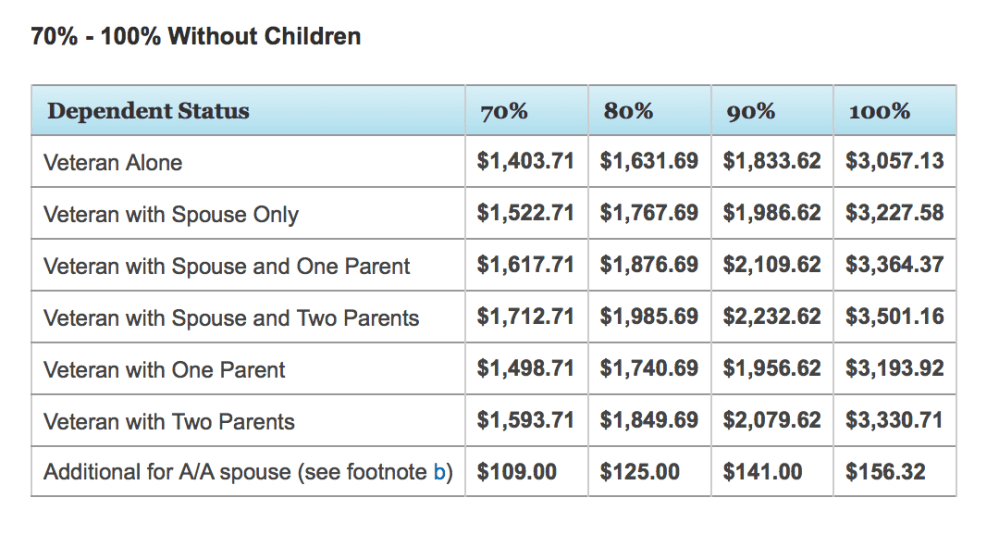

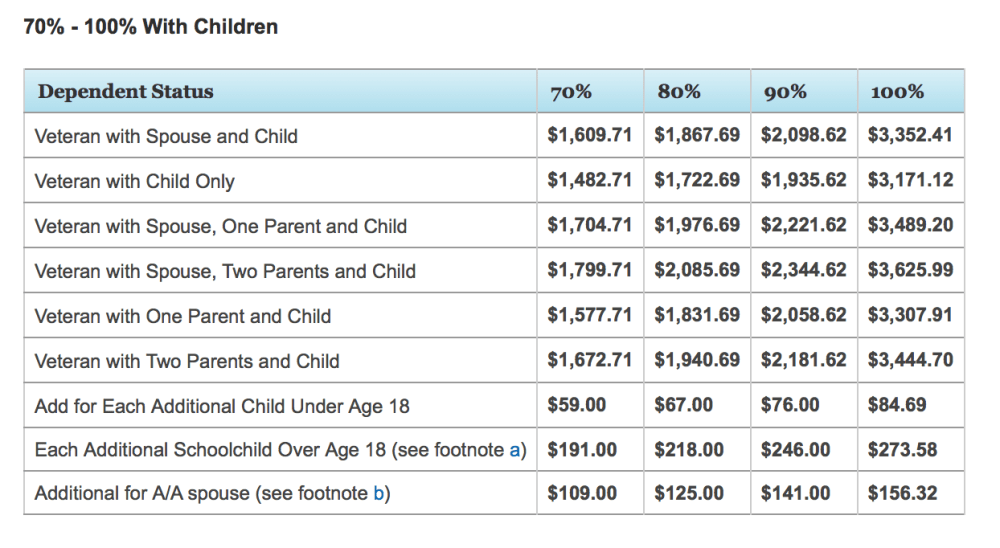

The above charts provide evidence our 100% disabled veterans receive an ample tax-free benefit designed to help them deal with their service-connected disability. Again, a disability (and disability rating) does not necessarily preclude veterans from being employable.

If I were to look at a family like mine with three family members, a veteran with his or her spouse and child receives $3,352.41 on a monthly basis. This family receives $40,228.92 annually, tax-free, and there is the possibility the family receives other forms of support, either earned by the veteran’s service (like a VA work study position), a civilian job occupied by the veteran, or by the spouse.

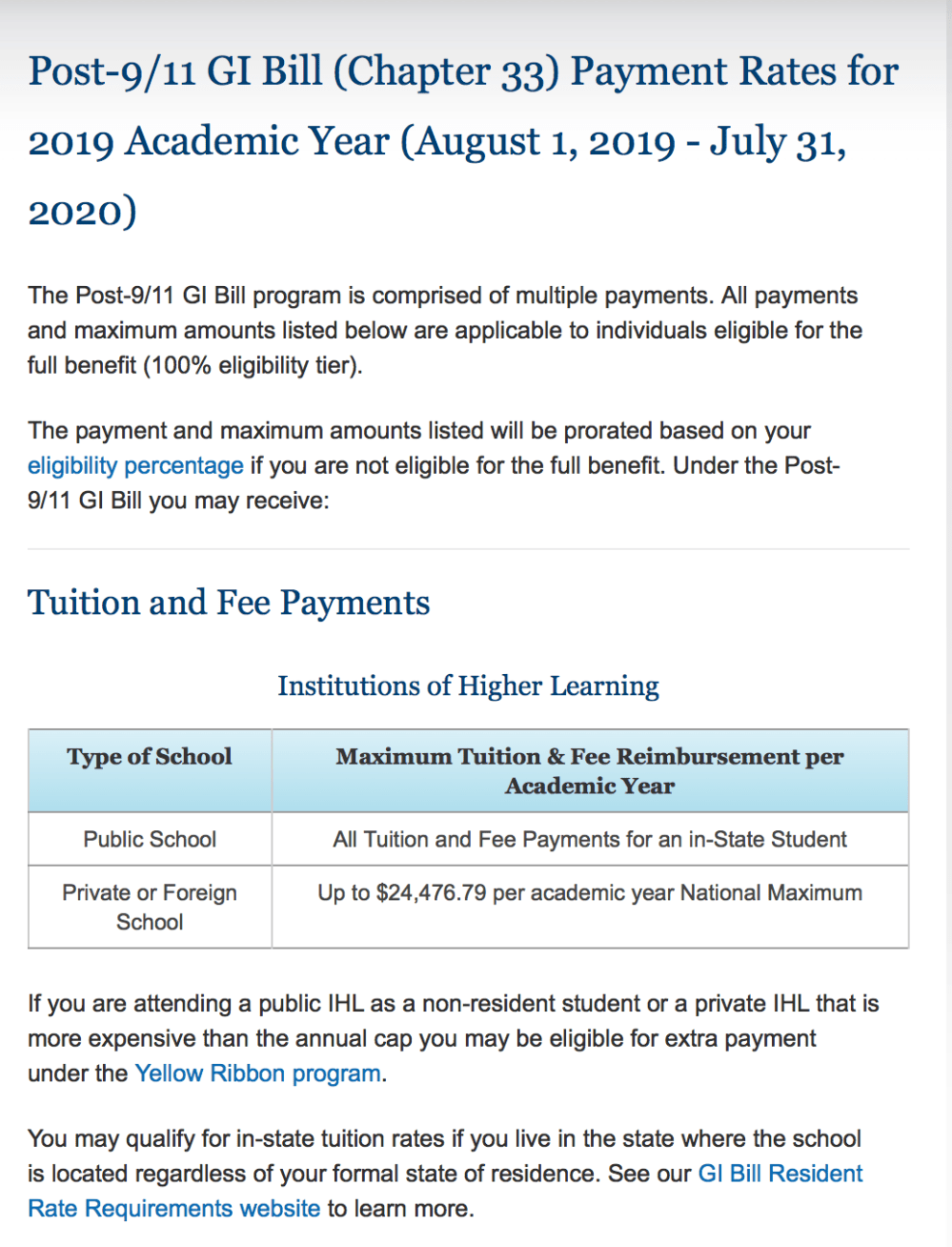

Many veterans are eligible for the Post-9/11 GI Bill and if they are eligible at the 100% level, their education benefits provide a significant incentive to not accrue student loans or to practice responsible borrowing.

Using Arizona State University as my example, having completed my Master’s there, let’s look at a few simple situations:

Spring 2019 (undergrad resident student, campus) $5,411

Fall 2019 (undergrad resident student, college fee 1–the cheapest programs) $5,669

The cost of this academic year is $11,080 covered completed by the Post-9/11 GI Bill. If we look at the Federal Aid max, a first year independent undergraduate can receive $9,500 in federal loans. Why take out the maximum federal loan when said student can take on work of some kind?

When I looked at the Federal Student Aid website, between four years of an undergraduate program, a student can take on $45,000. It might be easy to say that loan amount is needed for housing and other expenses, but again, the Post-9/11 GI Bill has other payments attached to it.

The basic allowance for housing varies across the nation for resident training but the Department of Defense rate, which started for student entering programs after 1/1/2018, is $1,680 for a full month of attendance at Arizona State University. If I recall correctly, there are between 113-115 days each for the spring and fall terms. The $1,680 BAH is divided by a 30 day month for $56 a day. If the term is 113 days, the student receives $6,328 and if the other term is 115 days, the student receives $6,440.

Plus the student receives a book stipend of up to $1,000 for 24 credits in the academic year.

Here’s a nice way to look at our 100% disabled (but completely employable) veteran:

$40,228.92 disability compensation

$12,768 basic allowance for housing

$1,000 annual book stipend

Total tax-free money cleared by student: $53,996.92

The rest of the money is paid to the school, but the $11,080 tuition and fees payment demonstrates the student does not need a student loan to pay for direct educational expenses unless the cost of books and supplies exceeds the book stipend, which it could. If anything, the student could have indirect educational expenses but he or she should modestly accept student loan debt instead of using the total and permanent discharge as a “get out of school debt” card because it is simply available. Other options are part-time or full-time work to pay for expenses not covered by VA educational benefits.

The VA also has another program called Vocational Rehabilitation & Employment. One of the tracks available helps pay for higher education which is what I am familiar with in my work. Like the Post-9/11 GI Bill, it pays tuition and fees to the school, the cost of books, and a subsistence allowance like the Post-9/11 BAH. Counselors sometimes pay for parking passes and consumable items, like paper and pens. It’s been a little while since I’ve dealt with this particular benefit on a daily basis, but the expectation is students must still provide valid support for incidentals.

Students can have either the traditional subsistence allowance for VocRehab which for a veteran and two dependents is $923.60 a month, falling back on my example of a family of three persons, or the alternative Post-9/11 rate for veterans who also earned the Post-9/11 GI Bill, paid at the same rate of the zip code of the school. In this situation the $1,680 monthly rate. I am not sure what percentage of VocRehab recipients in higher education are at the 100% disability rating, but I wanted to share this information for awareness purposes that our nation is already doing a commendable job setting veterans up for success without them having to seek the maximum student loan each year to fund their education.

I know I am barely grazing the surface of the issue, but I wanted to express why the matter of student loan forgiveness is not the same for a 100% disabled veteran with employability prospects as it is for the 100% permanently and totally disabled, unemployable veteran.

The first group can easily abuse the system set up to assist the disadvantaged and take out the maximum student loan amount each year, enjoying some $45,000 of fun money (from my example) with zero consequences unless a distinction is made moving forward that it is the 100% disabled, unemployable veteran community who should benefit from this collaboration and not both groups of 100% disabled veterans.

UPDATE (August 24, 2019, 5:42 p.m.)

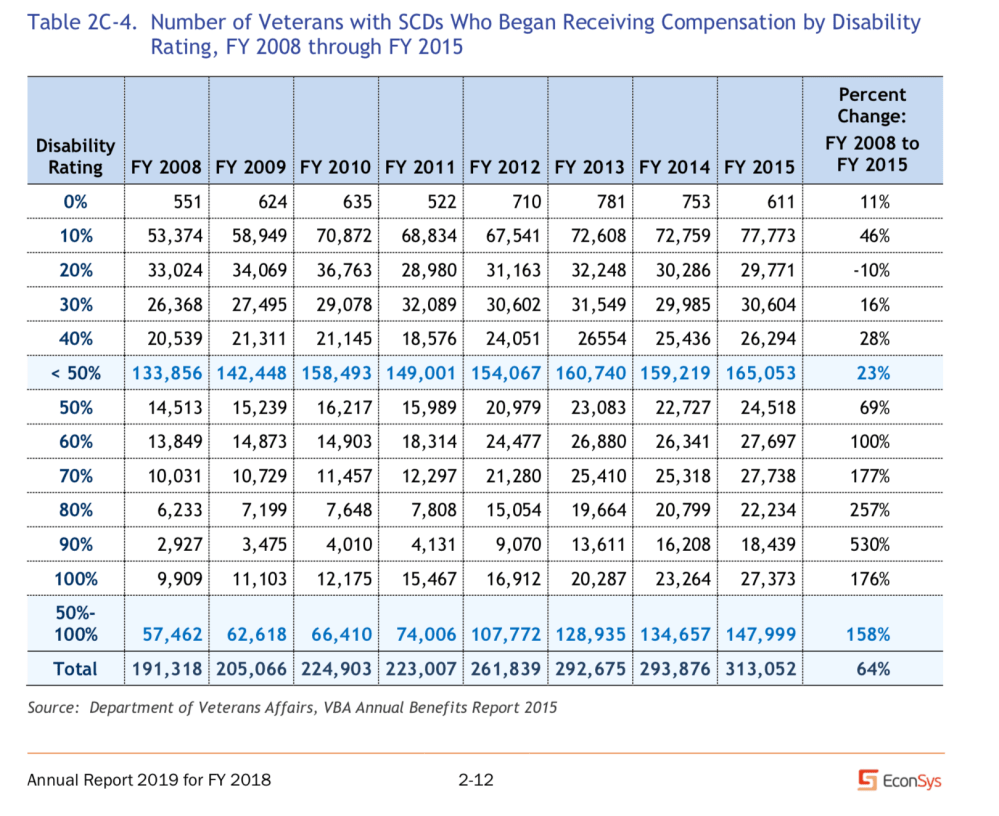

I meant to include this snapshot earlier when I was looking for some info on VocRehab to share. SCDs stands for service connected disabilities. The jump in disability ratings is a bit staggering for the 60-100% disability rating scale and it does shows the burden on the VA to attend to this influx in disabilities increased significantly. I pulled the information from the VA’s website. It just took a little Googling here and there to scout for VocRehab information that might be relevant for today’s conversation.

Like!! Thank you for publishing this awesome article.

LikeLike