Trick or treat, everyone!!!

I’m super excited to drop in today. October is my favorite month of the year and who doesn’t love Halloween?! My treat today was 2 hours off from work, so I’m spending it here catching up. Trust me, writing (for fun) is a treat for me, so I’m happy to be here sharing my thoughts.

Years ago, I promised I would finish my talk on using VA education benefits and although I dropped that ball for far too long, I am picking it up today and expanding on the topic of money talks. For some time now, I’ve listened to a number of finance podcasts. A lot of people have at some point talked about Dave Ramsey’s Financial Peace University, but the people I am most attracted to talk about the program as a starting point with the eventual goal of financial independence.

With these ideas in mind, today’s blog most is influenced by a variety of media that are pretty accessible. Something I’ve enjoyed reading from time to time is the Money Diaries series by Refinery29. I also love listening to michelleismoneyhungry and howtomoney.

So, what does the final tally of my 48 months of VA education benefits look like?

This funding helped me to turn around being unemployed and broke.

I graduated with two undergraduate degrees in 2012 and went through applying to 89 jobs before landing my first post-college position. Our lives in 2012 were pretty much as close to bottom as one can go. We had to move in with my in-laws and ended 2012 with $500 in the bank account. At that point, I was willing to take any job and that first post-college job sucked. My future boss in calling me in for a second “interview” told me veterans had not been successful in the position. To this day, she is still the top person who has made me feel being a veteran is a bad thing. The upside is her bad example of leadership had taught me how to crush it (again) in the workplace. I do believe there are individual veterans who set a bad example, but there are plenty of civilians in the same boat.

In speaking on those matters, it is important to discuss what I walked away from when I left the Marine Corps. It was the most serious job I’ve ever held and it has some of the biggest disparities between the best parts and worst parts of the job. As someone with only a high school education, I was doing fairly well for my income needs. The flip side was I had to deal with the aspect of losing my Marines, and later, the risk of losing my husband as he stayed in. I think when I was presented with the opportunity to stay in, my reenlistment bonus was on the low end, perhaps $5-$7 thousand and would have been taxed since I was stateside at the time. It was a good amount, but it was not enticing for the risk. I had to decide to leave behind a world where some basic needs like housing, food, medical, and dental were easier to manage and mostly or completely covered financially for the freedom associated with civilian life.

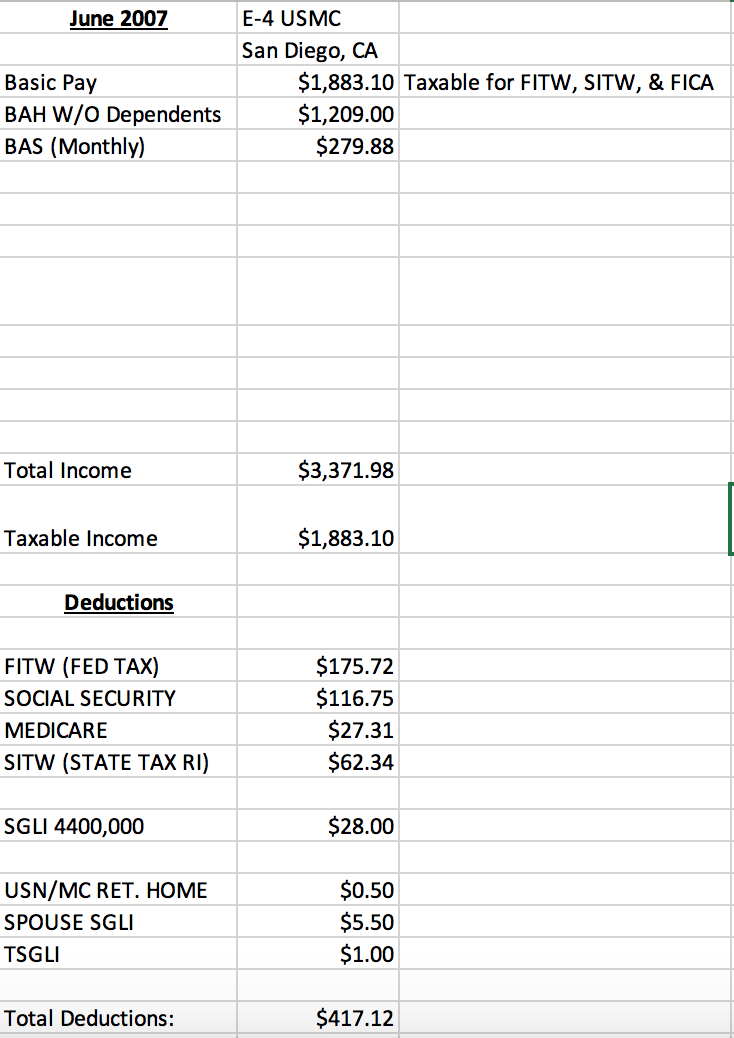

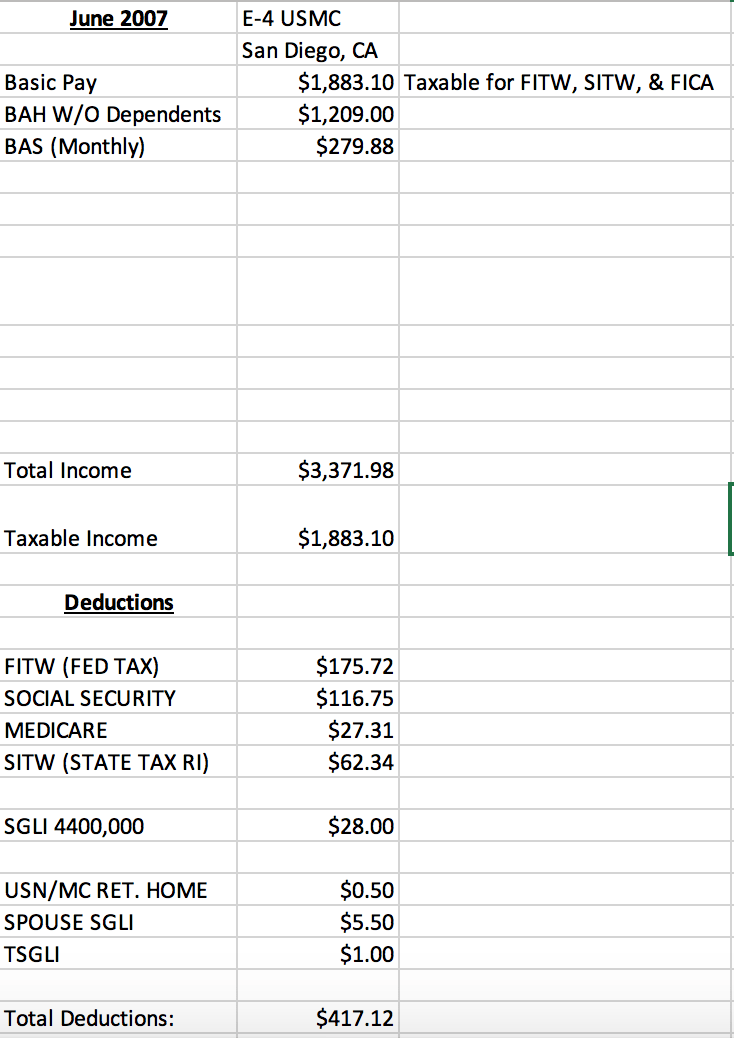

To give more transparency on this situation, I am providing details from a few of my Leave and Earning Statements from the Marine Corps and will also provide the comparison of my past employment with Arizona State University. For those that don’t understand the language, BAH is basic allowance for housing and BAS is basic allowance for subsistence (food).

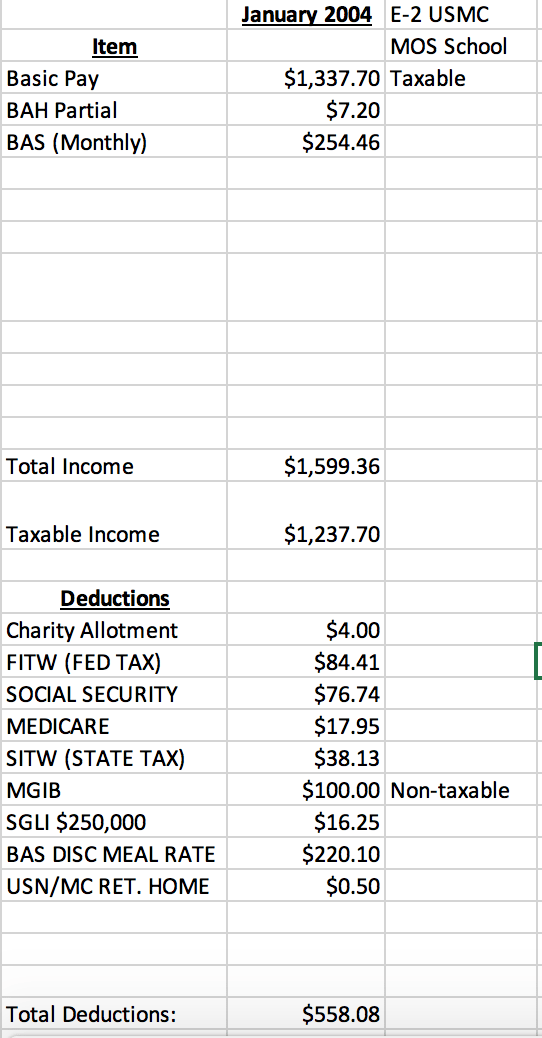

In January 2004, I was still attending my Military Occupational Specialty (MOS) school. I lived in the barracks room provided for me with two other women in my unit. We shared a rather simple room with a bathroom and had a common room shared with multiple other barracks rooms. I went to a chow hall (think college cafeteria for the closest comparison) for the bulk of my meals, except for the times I chose to grab food from the shoppette (We were training at an Army base.) or to go out for meals. The Marine Corps footed the bill for medical and dental bills, but at this time, I think the most I ever went to medical might have been for a cold.

As a young person with the bulk of my living expenses covered, no family to support, and no car, my only real bills were student loans and a cell phone. (I completed a year of college at Florida Southern College before becoming a Marine.) I’m pretty certain I blew all of my discretionary money on food…By the way, the MGIB is the money I set aside to earn my Chapter 30 Montgomery GI Bill benefits and I was a pretty lazy young person by not contributing to Thrift Savings Plan. I’m not sure what I thought about retirement goals at the time.

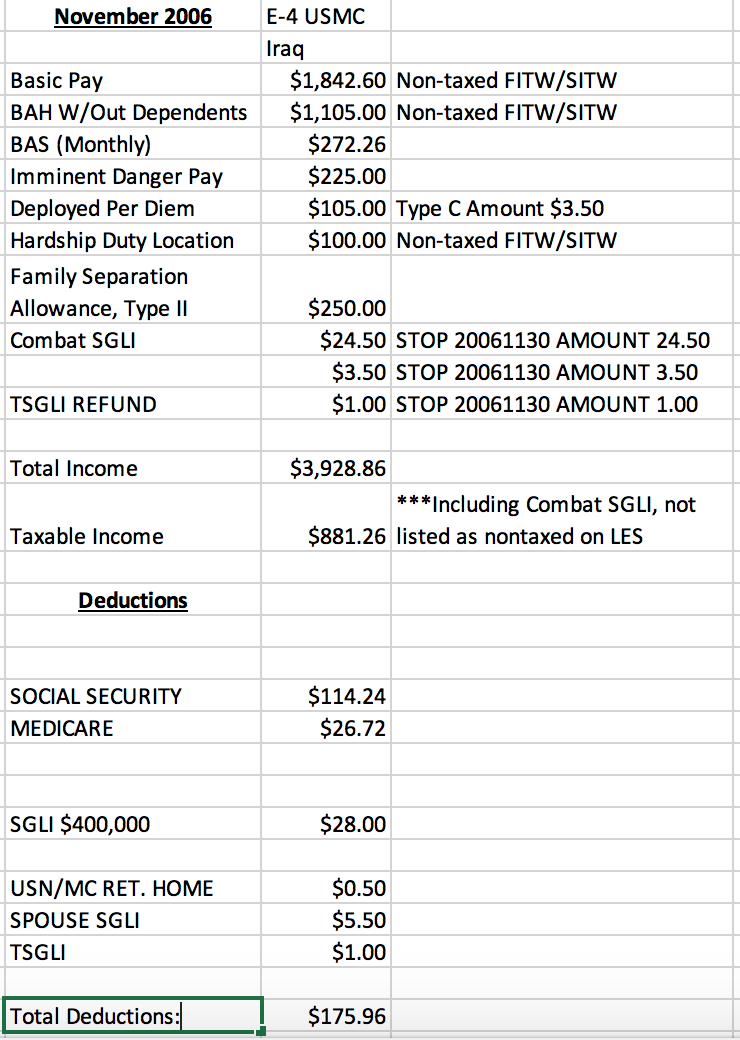

As someone who has gained financially from serving overseas, let me tell you deployment life has an upside. My second deployment was monumentally safer than the first and having married prior to deploying, we also started receiving a housing allowance to support living off base. (At the time, my husband established our household with a one-bedroom apartment I wouldn’t see until I came off of deployment.) I haven’t found an LES from my first deployment, but if I find one lying around, we can do a comparison later on. At the time, my husband and I had relatively few large expenses and as dual income earners with no kids, life was pretty great.

SGLI, for those not in the know, is Servicemembers’ Group Life Insurance. If I had died on deployment or anytime during my service after the higher rate was implemented, my husband would have received $400,000 from my life insurance. By comparison, during my first deployment, coverage was $250,000 and the funds would have gone to my parents as my primary beneficiaries.

Money is a big reason why staying in is enticing for service members. It was also a reason why my husband and I had a hard time in our conversations over whether I should reenlist or not. While I do think the military overall has become a more equal place for men and women, I didn’t feel that way when I served and I did not want to deal with the reality my husband and I might be on back-to-back deployment cycles. Towards the end of my Marine Corps career, my 7 month deployment overlapped with a yearlong deployment for him and as a result, we missed out on seeing each other for most of the first 16 months of our marriage. That experience, and a few others, provided the necessary knowledge that money isn’t anything, but it is something to be leveraged.

It did not take long to figure out we had to fend for ourselves. When I was not kept on in my first post-undergrad position, I had to empty out the retirement contributions I made over those six months because Arizona was so far behind with respect to its unemployment office I had to wait for three months before even being considered. (Luckily for me, I was hired by Arizona State University just in time.)

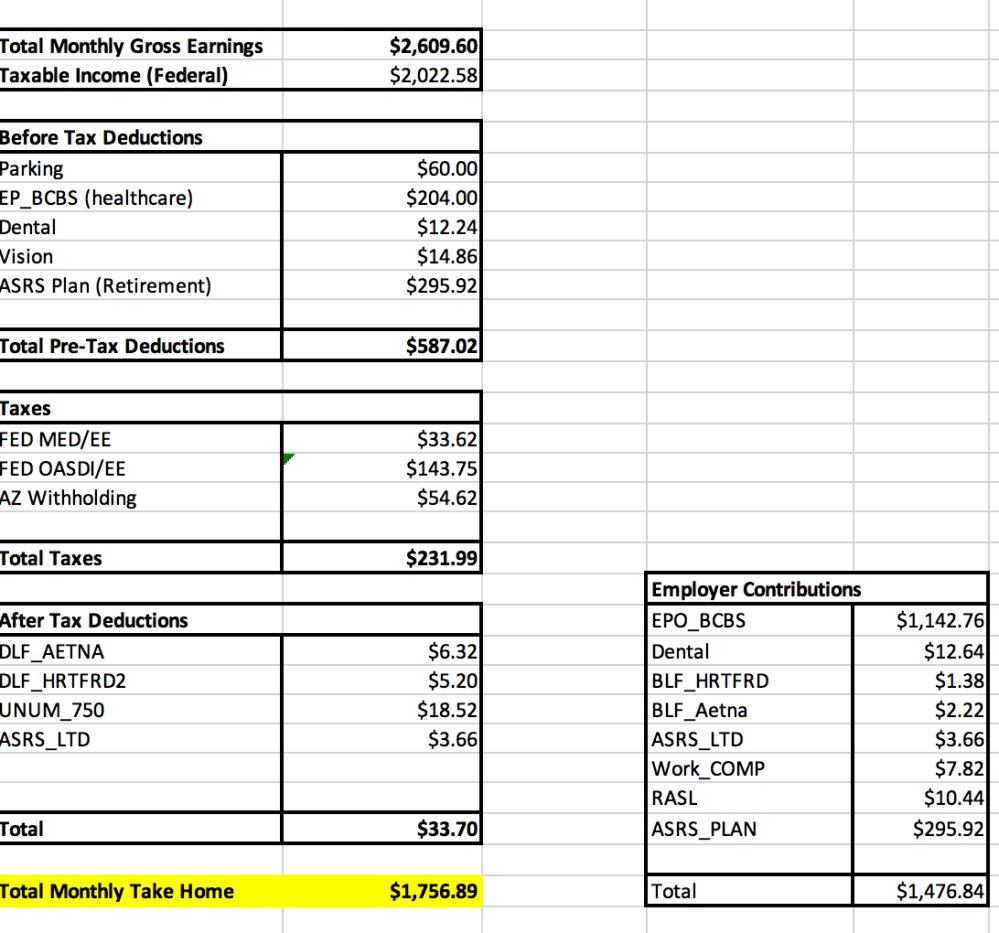

My next career move was quite a humbling one financially. If I had stayed behind in public health, my yearly gross income would have been approximately $48,900. Switching to higher education meant starting at $32,500. When I left in 2017, I was making $33,924.80 or $16.31 an hour. The position has since been reclassified, resulting in more pay for my peers. At the point I decided to leave ASU, I needed to easily increase my take home pay and one of the best things immediately available to me was picking a position that did not pay into Arizona State Retirement because I was contributing 11.6% a paycheck. As beneficial as it is to contribute so much to retirement, I was the only income earner and I felt comfortable taking a temporary reduction in retirement contributions to benefit our longterm goals.

Thankfully, the power I gained through using VA education benefits provided the cushion I needed so I could move on without dipping into retirement funds two years ago. For anyone, I would recommend avoid pulling your retirement contributions if you can because you get taxed on it pretty badly and I don’t remember what penalties were in place. The biggest downside for me when I left ASU was that I lost out on the employer match for their contributions because I was not fully vested.

From one of my last months with ASU, here’s how things broke down:

When I left the Marine Corps, I never imagined I would make less in 2017 than I did in 2007. This is why I want to show how beneficial VA education benefits are to making a successful transition and I want to encourage those who have benefits to use them wisely. When the money is used up, it’s used up. You’ll end up with a completed goal or wish you had. The only caveat I make with the rudimentary list I created below (Sorry, my Excel skills leave something to be desired.) is that I did not work a full year with ASU in 2017. Instead, I wanted to show what my year would have looked like had I stayed. As a reminder, I am showing the total income not the take home income for the year.

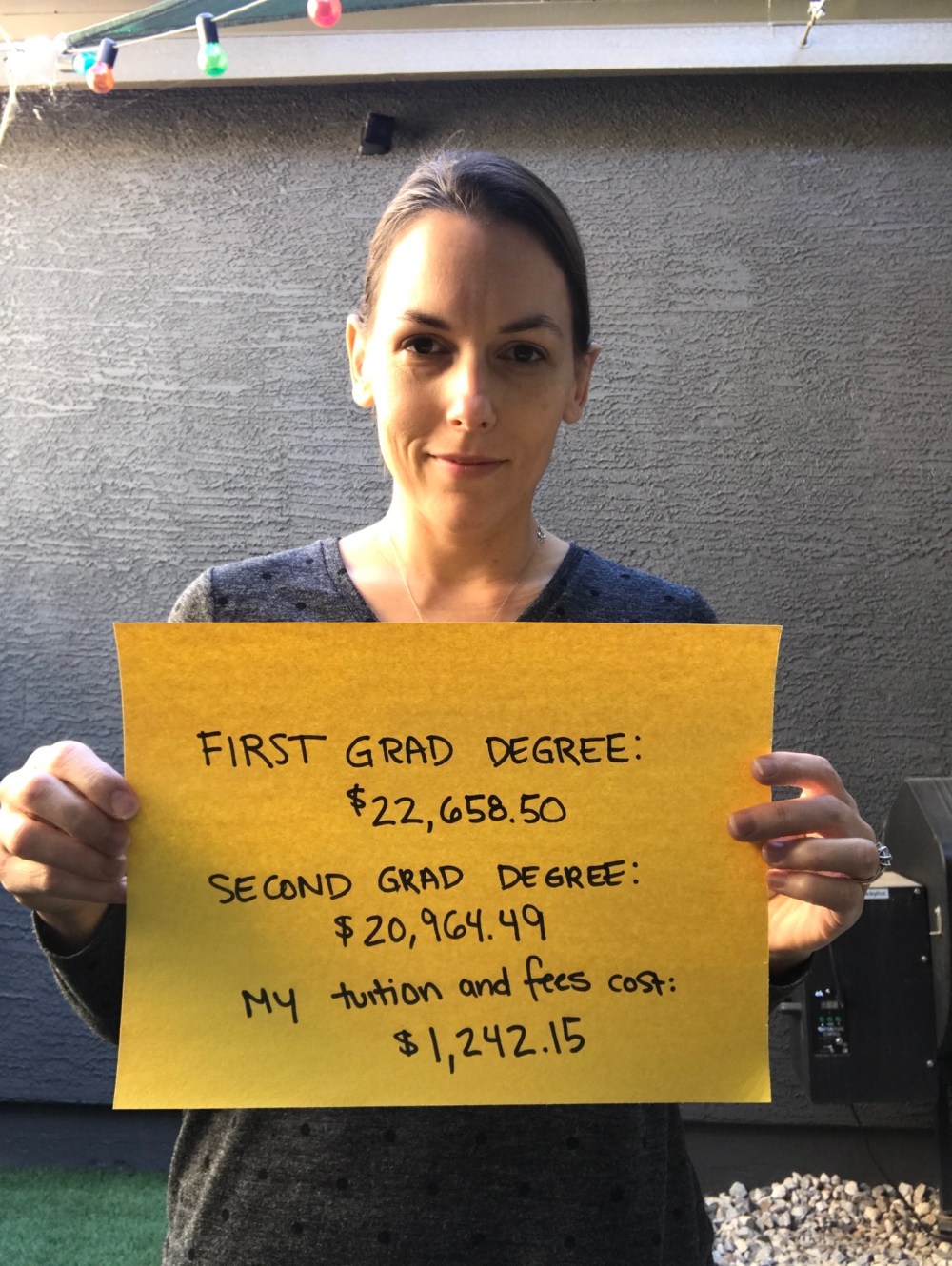

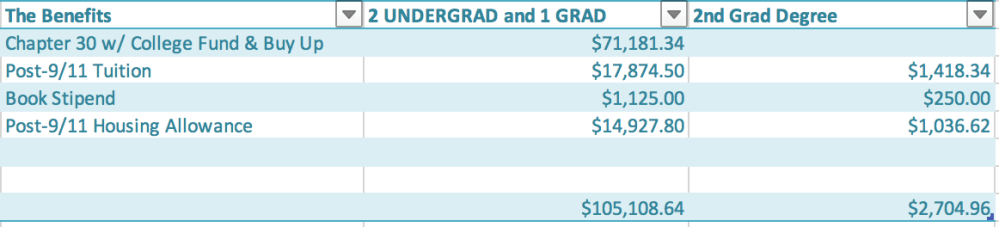

I have made substantial progress from having almost nothing in 2012 to where I am today. My Chapter 33 benefits paid for $17,874.50 of my MA in Social and Cultural Pedagogy program with ASU’s employee benefit covering $4,548. My portion (the fees for the Fall 2015 term when I used the employee benefit) were $236. To pay only $236 directly for a $22,658.50 graduate program is pretty amazing.

To also move on to a second graduate program which costs $20,964.49 and to “hack” it the same way allowed me to accomplish something I never thought possible. The VA paid $1,418.34 towards my MPA program, my employee tuition benefit covers $18,540, and I am paying the remaining $1,006.15.

Lastly, my benefits greatly reduced my need for student loans, but I do have some to tackle after my program ends in November. We’ll talk about those a bit later down the road.

See you all next month.

~Cheryl

P.S. If there are any math errors (or glaringly obvious typos), please be kind in pointing those out. I stayed up late yesterday to complete a paper. Thanks!