GI Bill® benefits are my topic of discussion today and more specifically, I wanted to talk you about my own benefits. My education benefits are a significant reason why I am successful today in my educational pursuits. I have accrued some student loan debt, which is (always) a personal choice. This post is NOT about recommending student loan debt to anyone as a means of affording a college education.

Debt (of any sort) has significant consequences. I went into default on one student loan during the timeframe of my first deployment. It was the only loan I did not get deferred prior to deploying. Instead, I asked my dad to pay my loans using my bank account information. While I was away, he had trouble accessing my account and no payments were made. As a direct result of my pre-deployment and deployment situation, my loan went into default. I was greeted with nasty collector phone calls upon my return stateside and a short while after returning home, the majority of my deployment savings were eaten up by the debt payoff. It took seven years to get this crappy stuff off my credit report.

Now, I still have some undergraduate student loans to pay and a modest amount taken out while I’m attending graduate school. There are–and always will be other options–to pay for non-tuition related expenses associated with school and life. My decisions to take out those loans (and any loan in my future) are specific to me and should never influence another person to decide taking out loans are right for them.

I went through Dave Ramsey’s Financial Peace University a few years ago and I am working towards a debt free life as best as possible. Will I “slip up” here and again? Yes. Trust me, if you were ever to see how crazy my grocery bills are at times, the answer is ‘yes.’ Will I also make the choice to take on some forms of debt? Yes. My decisions though will be better researched and more deliberate. Debt will be treated like a condiment rather than an entree in my life, if that helps make sense to anyone questioning my approach.

For my current state, my GI Bill® benefits help tremendously in my financial planning. After a yearlong unemployment in 2012 and the second bout of unemployment in 2013, my family’s finances looked scary. A significant turning point in our lives after gaining employment with Arizona State University was my decision to start a graduate program sooner than originally planned. I had 13 days of the Montgomery GI Bill® remaining and upon exhausting those benefits, my 12 months of the Post-9/11 GI Bill® could kick in to pay for my education.

This newest chapter of education benefits is pretty amazing. My tuition and fees are covered at 100%, I receive a housing allowance (when applicable), and I receive book stipend money. The tuition and book stipend money are great by themselves, but the housing allowance is that extra something that mattered greatly in reestablishing my family’s finances. My husband also receives a housing allowance through his use of the Post-9/11 GI Bill®. My housing allowance has become my family’s supplemental income. Currently, my husband not working full-time while he works on his undergraduate degree. This is a necessary arrangement for my family to avoid unnecessarily high before and after school care for our daughter. We will incur those expenses again starting in the fall once he starts his law degree (and is not permitted to work that first year).

For this semester, I used ASU’s tuition waiver. If my family was less dependent on the Post-9/11 GI Bill® housing allowance, I could have certified less credit hours each semester to 1) cover my tuition in full and 2) avoid being taxed for using the tuition waiver. Once again, my decisions are intentional and appropriate for my circumstances. I am not a financial advisor so what works for me, may not be appropriate for others to follow.

So, would you like to know how much I’ve benefitted from those GI Bill® benefits? The numbers might surprise you.

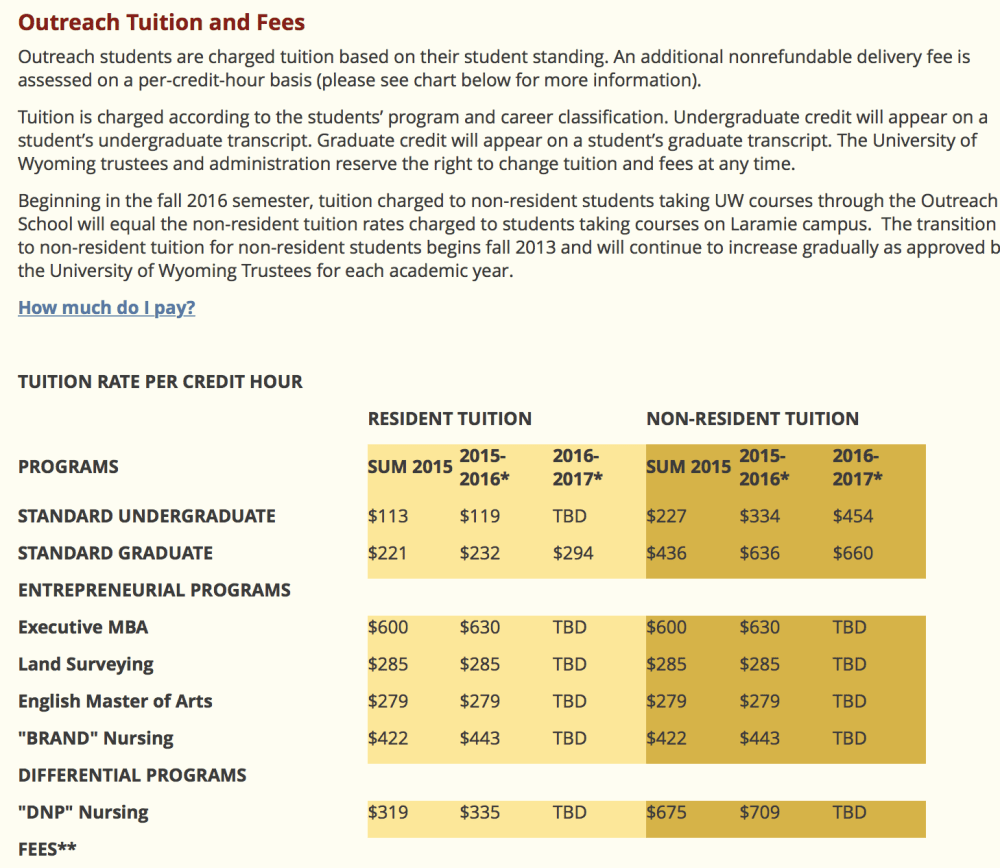

Below is an example of University of Wyoming’s costs for its Outreach Program. I am a little too lazy at this moment to sift through my bank account statements from 2009 to 2012 to tell you specifically what it costs me to get my two Bachelor’s degrees. This information is good enough for my illustrative purposes today. While I was attending University of Wyoming, I used my Montgomery GI Bill® benefits. This type of education benefit is paid flat rate based on training time to students and students, in turn, still pay their institutions for their semester expenses. I’m oversimplifying the process here, but current payment rates are available here if you’re interested in learning something new.

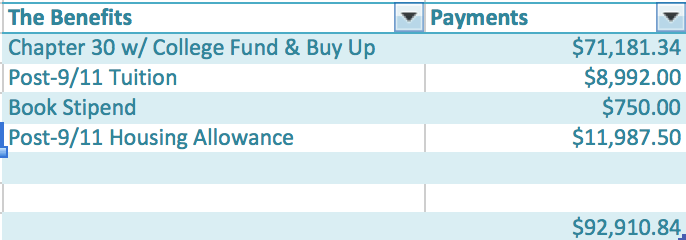

I made a conscious decision after the Post-9/11 GI Bill® came into being that it wasn’t right for me at that time to relinquish my Montgomery GI Bill®. Given the lower cost of education (and housing allowance) in Wyoming and the fact my education benefit was supplemented by the Marine Corps College Fund and the $600 Buy Up Program, I would have lost money converting over to the newer benefit earlier in my education career.

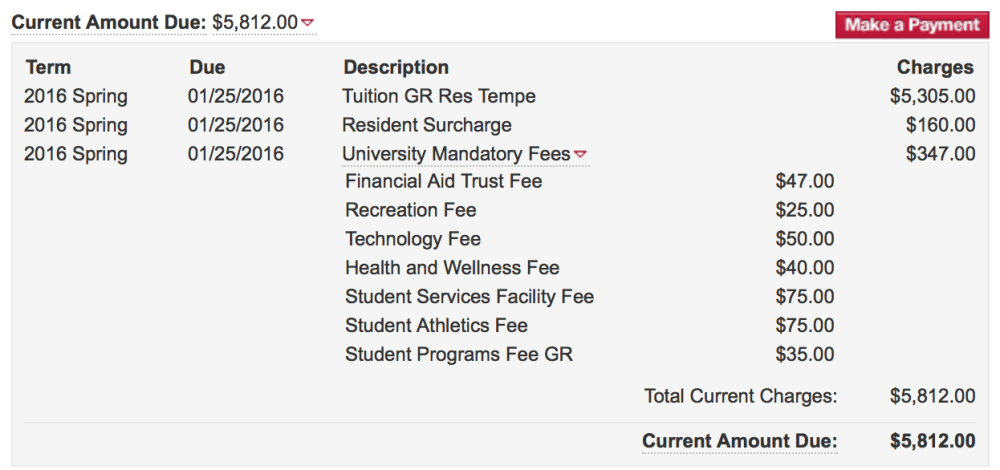

Instead, I had the financial freedom to earn two Bachelor’s degrees and pay 4 of the 5 semesters of my current Master’s degree with thePost-9/11 GI Bill®. The earlier numbers of my disbursements do not yet factor in spring’s tuition and fees (listed below for your convenience), my housing allowance payments, or the book stipend money. At the end of this program, I will still have roughly 1 month of Post-9/11 entitlement to spend on a future education program.

My graduate program might seem expensive to some, especially given those earlier numbers reported for the University of Wyoming Outreach Program.

I am privileged to work for Arizona State University, which played a role in looking at schools. More importantly, my particular graduate program is the only one of its kind in all of North America.

Each and every day I am thankful large sums of educational debt do not stand in the way of my current and future dreams. My GI Bill® benefits make this reality possible.

I owe gratitude to everyone who played a role in establishing (and maintaining) veterans’ education benefits, both past and present. I am thankful for the recruiter, SSgt Killough, who sat down with me and told me the College Fund was available as an enlistment incentive. I am thankful for my command at my first unit; along the way there, I learned the Buy-Up program was possible and I paid $600 to earn higher education payouts later. I am thankful to the teams of people who process my educational benefits.

My lifelong outcomes are greatly improved because these benefits exist. I am the first of my siblings to graduate college with undergraduate degrees and in spring, a graduate degree. Those strengths will shape and mold my daughter’s educational attainments and the lives of her friends and peers that enter our home. My family’s wellbeing is greatly improved in the short term while we are not fully a two-income family. Every additional dollar of my housing provides an additional dollar to pay for healthy groceries, pay for recreational activities, pay off debts earlier, etc. Society is better off as well as I return my educational investment back into the workforce in how I coach and support others in the community.

For anyone who is thinking of not using his or her education benefits, I’m curious. Why lose out on the money you’ve earned? Why deprive yourself of a self-improvement opportunity?

Keep learning about who you are and what you want out of life. Build an understanding of your GI Bill® benefits and use those benefits to propel you into the future vision you have for your life.

~Cheryl

One thought on “VA Education Benefits: 48 Months of Money”