I wanted to share some thoughts on a podcast I recently listened to because it’s on the issue of money. I listened to it maybe a week or two ago and it was hard to imagine not sharing it. (In fact, I’ve already shared it with a friend and felt more people could benefit from it.) Although the intended audience for this episode is service members and there’s guidance for veterans, too, I think the message can be encouraging for everyone to work on building their personal savings or just check out any of their other episodes for inspiration.

I want to share everything is my own viewpoint. I am not writing on behalf of anyone I’m discussing today. I am also not writing in any way related to my employer since some things I want to share are related to the higher education industry. I do not receive any financial gain from anyone, but I found these tools useful for my purpose and I feel others might as well.

Current readers know I’ve made some poor money decisions, been unemployed, and found having the Post-9/11 GI Bill, earned through my military service, has changed my life. Some have also read my thoughts on using Dave Ramsey’s baby steps to improve my financial situation. This entry is along that same vine. More recently, I’ve picked up other tools for my financial toolbox: podcasts and a new budget book.

I didn’t imagine I would get into listening to podcasts. I’m not entirely sure why because my mom used to listen to motivational tapes when she drove my sisters and I to school. I think I thought they weren’t something I needed. Mostly, I listen to music at work but a coworker mentioned listening to podcasts and by chance one day, I found out some of Refinery 29’s Money Diaries are available on podcasts. I know it shouldn’t be that exciting to me, but reviewing some of these money diaries where these women (and sometimes their partners, too) make substantially more money than I do is a form of social education. Money shouldn’t be a social taboo to talk about because we have the ability to harness our money better and we haven’t always been taught how to make those decisions. I have listened to other ChooseFI episodes, Millennial Money, and Bigger Pockets Money, which from one of their episodes is being rebranded Wider Pockets.

I am certainly one of those people who was a bit late to making informed decisions about money. My friends, Jacquie and Ken, introduced my husband and I to Financial Peace University and it was the first step in the right direction. Our daughters are a month apart in age and by learning of their money story, we were free to say, “Hey, this is my money hurdle right now.” We had carried some serious debt with us from our time in California and took a money hit when we moved to Wyoming. I think this is the first time I ever truly discussed money with my friends and to be honest, it wasn’t easy. Their support was an important stepping stone and they are still great friends to this day. I wish I kept better notes when we were doing FPU but we managed a $9,585.10 turnaround in 91 days by exhibiting some discipline. We started the program January 2011 and by the end, we saved $1,839 and paid off $7,746.10.

This podcast episode is something I could have used during my four-year Marine Corps career. My career was a missed opportunity to save like crazy since we were just a family of two and before then, I made the decision to not commingle my money while dating. I just wasted my money on stuff like clothes, a computer, snack foods, and dining out. The only responsible thing I did was pay off my student loans. I know the opportunity to save like crazy is still available here and now, but it will look different. I don’t have free health care and dental as I did in the Marine Corps. I don’t have a housing allowance like I did on active duty. I don’t have any GI Bill benefits remaining. The awesome thing though is I am in a great position to earn more money as my career progresses and soon enough we’ll have a second income again.

I won’t completely unpack the episode from ChooseFI because I think that does a disservice to other listeners, the hosts, and the interviewee, Military Dollar, but there is an observation I have from personal experience. The implementation of the Forever GI Bill and the removal of the delimiting date–opens up a great window of opportunity for Post-/911 GI Bill students. (Note: The delimiting date is still applicable to certain recipients, but if you’re interested in learning more, check out the VA’s website.)

As a veteran who has used Chapter 33 benefits, I think the removal of the delimiting date will help cut down on the number of veterans and eligible family members who feel pushed into school before they are ready for higher education. I think if people feel more comfortable taking their time and understanding their personal and professional interests, they will–by and large–make more informed decisions about their schooling and perform better academically rather than flunking out and exhausting benefits before earning a degree.

The other gain I see is the ability for veterans and eligible family members to conserve their entitlement for graduate programs. Some of what I’ve heard in listening to money podcasts is community college as a “life hack” and while I wouldn’t call it a life hack, I do agree it’s a smart investment. Community college is a cost-effective measure to reduce the expenses. (I’ve done it so I’m not just spitting out words here.)

Saving Chapter 33 benefits would be another “life hack” if we want to call it that for the purpose of today’s discussion. When I completed my undergraduate studies, I did not imagine I would ever attend grad school but that door opened up for me. Knowing this information now and as I complete my second graduate program, I love encouraging others to make more fiscally responsible decisions in regards to their education. Although I am no longer an Arizona State University student, I want to use their tuition and fees structure to make my point about maximizing the Post-9/11 GI Bill; that’s where I got my first graduate degree from and just to clarify, this discussion does not translate equally to private institutions as the VA has a tuition cap per academic year for private and foreign schools. Starting August 1, 2019, the tuition cap is $24,476.79 and if you’re interested in more info on VA education rates check out va.gov.

In this situation, we will imagine a veteran student who is at 100% with 36 months and 0 days remaining (i.e. a student starting fresh in his or her program.) This situation also assumes a student certifies for full enrollment each term. For simplicity purposes, I’m acting as though no other forms of financial aid are being utilized.

- The student would receive book stipend up to 24 credits in an academic year ($1,000).

- The student would receive the Department of Defense rate for housing allowance; ASU’s rate is $1,602 a month for a full month of attendance. (Eligible students using this benefit before 1/1/2018 had a higher BAH rate. Partial months of attendance are pro-rated.)

- The student would receive tuition and fees covered to the highest in-state rate.

The undergraduate example uses Ira A. Fulton Schools of Engineering programs at the Tempe campus:

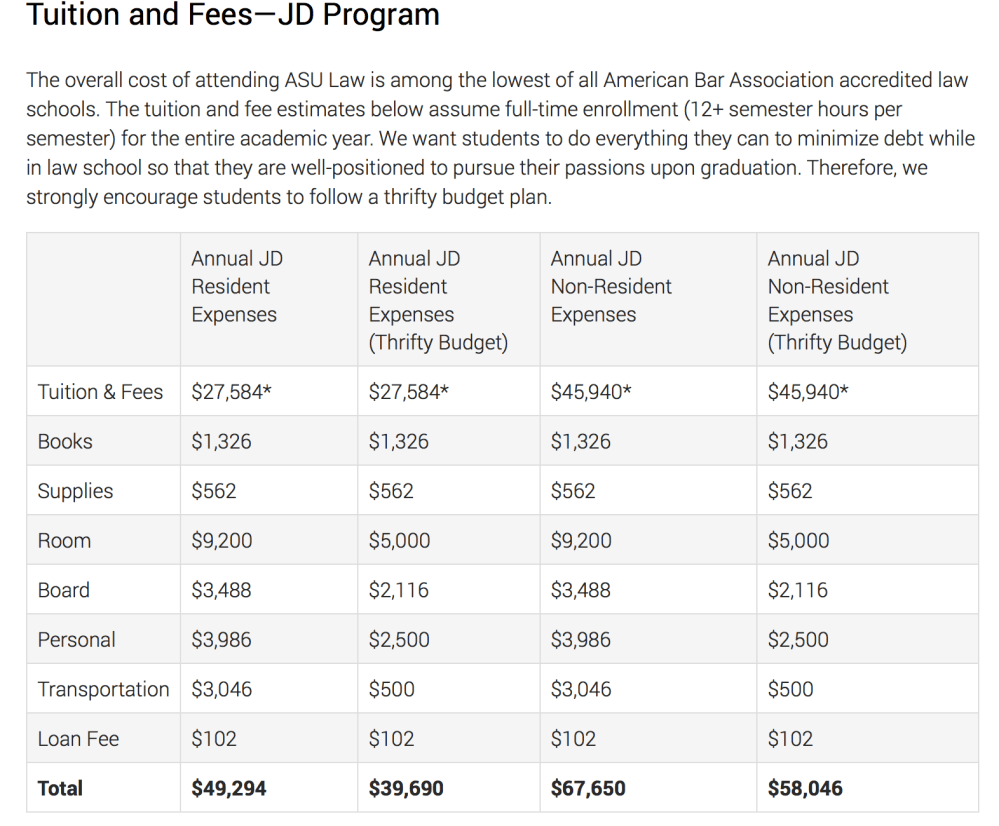

Here’s the Law program information:

It doesn’t take much to look at the cost of the law school tuition and fees to see why–for most students–if they can, they should reserve an appropriate level of benefits for their most expensive program. In most cases, that’s likely to be for grad and professional degree programs. A traditional term is sixteen weeks, so we’re talking approximately 4 months of entitlement per semester. A three-year program, like the JD program, uses approximately 24 months of benefits leaving the student the opportunity to have 12 months beforehand at the undergraduate level program.

I want to take a moment again to compare the fact the VA can pay the tuition and fees for this student at the JD level for ASU, a state school, although the total expense exceeds the tuition cap for private schools of $24,476.79 regardless of undergraduate or graduate program of study.

It’s just some food for thought I wanted to share given the fact if we had found ourselves in a better financial situation when my husband returned to school in 2012, we also would have been benefitted in the long run to conserve benefits for his law school program.

Non-veterans could find something similar with employers who offer tuition reimbursement. They wouldn’t get the benefit of a book stipend and housing allowance like what’s attached to the Post-9/11 GI Bill, but it’s a good place to start to avoid accruing student loans or to reduce the overall portion of student debt.

The other tool I started using recently is a new budget tool.

We are only a few months short of us returning to being a dual income family and I want to just kill it on tackling debt, building savings, and contributing to our retirement. I like the teachings of Dave Ramsey but I am interested in changing things up a little to suit us better. I like the concept of the zero based budget Dave preaches but I didn’t like all the categories of the FPU budget so that’s why this book is particularly appealing to me.

Once we both are working, my goal is to maintain our monthly budget at our current spending. The big change for us is holding off on buying a new house so we can have a yard instead of an 11 by 17 patio. While we’ve wanted a more suitable home space for entertaining, it’s logical to stay put so we can snowball our debts sooner. We are also fortunate the home we own is in good shape and we have some equity in it which will allow us a cushion leftover post-sale. I also think if we avoiding falling back into over consuming, we can enjoy our careers more. With this goal in mind, we will take some inspiration from the intense focus in the FIRE movement. We’ve discussed not fully embracing FIRE (Financial Independence, Retire Early) but we are onboard with being more intentional with our money. I found it interesting to learn the opposite of the debt snowball (starting smallest debt to largest) is the debt avalanche (starting with highest interest down to smallest) and as I explain below, our option is to pick a middle ground between the two. It’s clear the new budget tool/FIRE inspiration/Dave Ramsey Baby Steps as a combo is worth testing out to see how we like it.

This past month, I noticed we fell back into overspending on dining out. I think taking the idea of “money envelopes” again from Dave Ramsey is important for this budget category as it is our Achilles heel. We did do better in other categories like spending on gas and grocery shopping. I am being more intentional buying meat on sale and relying less on recipes. It’s easy to cut back at least $20 a week by reducing meat consumption and by using less recipes, we are cutting down on food waste. Thankfully, we all also like simple entertainment on a regular basis like being outdoors and riding our bikes, walking around the neighborhood, and watching shows. This lifestyle keeps our entertainment budget low without feeling like we’re deprived. Our longterm goal of serious travel will be something to save up for, but we’ll make our first trip happen in the next few years.

The last thing I wanted to talk about today is another deviation we’re taking away from the baby steps in FPU. This is my middle ground between the debt snowball and the debt avalanche. Baby Step 2 is to “Pay Off All Debt (Except the House).” We owe less on our house than we will for my husband’s education so we’re switching these around. I’m not sure how other people might feel about it, but especially after the housing market crash, it’s better to pay off the house first in our opinion than those loans. It’s not like the law degree could be taken away due to failure to pay but according to Business Insider, nearly 10 million lost their homes due to foreclosure during the housing market crisis. I’d rather have a paid off roof off my head and those student loans sticking around a bit longer, so that’s the plan.

If you’re not familiar with Dave Ramsey’s 7 Baby Steps, here they are:

- Save $1,000 for your emergency fund.

- Pay off all debt (except for the house) using the debt snowball.

- Fully fund your emergency fund (3-6 months of expenses).

- Invest 15% towards retirement.

- Save for the kiddos’ college. (If you don’t want to have kiddos, let’s move on to step 6.)

- Pay off your home early. (Don’t want to own a home. Let’s move on to step 7.)

- Build wealth and give.

Thanks again for dropping by. I’ll check in with you all again in May.