We’re all going to die some day. It’s not something we enjoy talking about–or planning for–but it will happen. Some of us have short times here on earth and others live well into their 100’s. Planning for the inevitable falls on us–or for those of us too young or indigent–someone else must plan and set aside funding for burial expenses.

Normally, I would not write about such a topic. People don’t really like being reminded that they are going to die or that their loved ones will eventually die. I am with you all in this regard and more so because of how often death has touched my life starting with my mother’s passing in 2000. Death, though, has not stopped there.

On my first deployment, my family tried to spare me this burden and delay notifying me my Uncle Duke passed away. On this same deployment, my dad’s (stepfather, legally) father passed away. My work also suffered the burden of losing one of our own, Captain Brock. I didn’t think about what difficulties my family members may have undergone if sufficient life insurance was not in place, because it’s not something we (and certainly, many families) discuss or want to discuss.

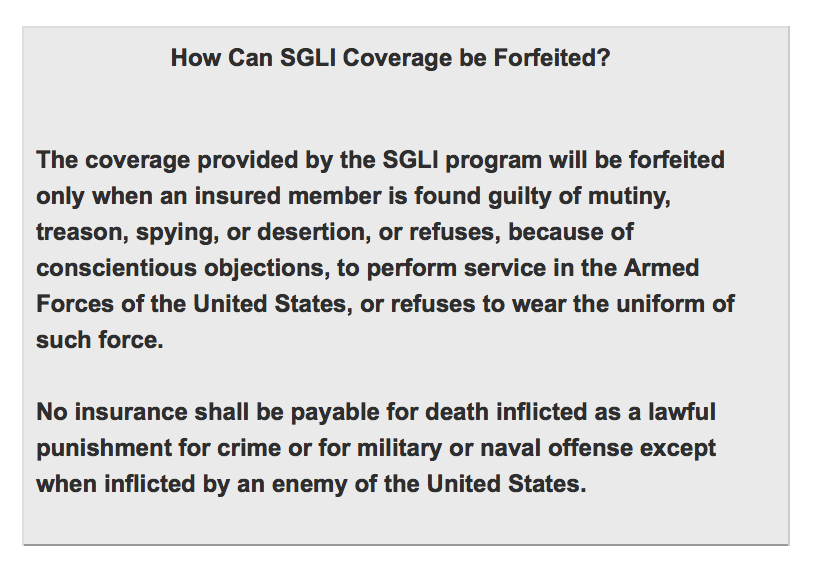

I didn’t think of what arrangements Captain Brock’s wife made for him; thinking back, I’m assuming he had the maximum Servicemember’s Group Life Insurance, which is $400,000 and he may also have been covered under the $100,000 Family Servicesmembers’ Group Life Insurance. My husband and I had this spousal coverage on each other while we were both active duty.

As active duty service members we each had $400,000 worth of SGLI, although when Bart was killed in 2002, his mom told me his SGLI had been $250,000 and unfortunately, from her, I learned his parents were not listed as beneficiaries which meant paying for his burial costs without this financial support. I don’t know about all life insurance plans, but ours recommends reviewing the beneficiaries at least one a year. Based on my conversation with Bart’s mom, I made sure my parents were listed as my beneficiaries when I was single or dating because they would bear the costs of my burial. I didn’t update this information again until I was married. It was updated yet again when we had my daughter. Should we later adopt, I would update my plan again.

When individuals get out of the service, they can get Veterans Group Life Insurance up to the maximum amount of SGLI they had while serving.

I imagine someone on the outside would assume these numbers are unnecessarily high, but life insurance can help with more than just the bare necessities of funeral planning and for many people, life insurance that just covers burial costs is not enough. Inadequate life insurance and no life insurance at all can be devastating for people who lost their family’s sole (or higher) source or income. The Granite Mountain Hotshots’ lawsuit settlement is just one example of why life insurance planning is an absolute necessary.

However, this conversation is not limited to just replacing an adult’s income. When I worked for Pinal County, I had the privilege to learn a little, informally, about the handling of birth and death certificates. A peer there told me about the life insurance policies she has for her children. I also carry a policy for my daughter, so we would not be financially crippled should the worst happen and we are faced with her burial costs.

The reason I decided to write on this subject today is because I learned via Facebook a 2003 graduate from my high school recently passed away. I do not know the circumstances of his death, but his family is struggling to pay his funeral expenses. Given his age–thirty years old–I wonder why he didn’t have life insurance. Did he think it wasn’t necessary? Was he barely scrapping by? A donations request was sent out and donations are coming in to help reduce the burden on his family, but I wonder if it will be enough.

Depending on what options a family explores, burial expenses can be overwhelming (funeral, travel, flowers, etc.). I took a personal finance class with the University of Wyoming and the following from Garman and Forgue’s Personal Finance (9th ed.) is a useful needs-based assessment:

-Final expenses

-Income-replacement needs

-Readjustment-period needs

-Debt-repayment needs

-College-expense needs

-Other special needs

*Add all these totals together and subtract government benefits and current life insurance assets to get the total life insurance needed.

And while I don’t feel like tackling the whole life insurance and term life insurance debate, I will say I purchase term life insurance. It’s just appropriate for my life right now. My premiums are not ungodly which is great since my paycheck is smaller than what I made while on active duty. My last premium, in fact, was due the day I learned this former student had passed away–if this new is not an incentive to get life insurance (or to make a timely payment), I don’t know what would be.

When I die, I know I want a simple service and I want to be cremated. I think it’s such a waste (for me anyways) to have an elaborate casket and flower arrangements. Cremation is less costly and I’m not a big fan of flower arrangements. After my mother’s death, our house was littered with so many flower arrangements. These beautiful things competed with each other–in small bunches, they smell beautiful but the combination of them makes an odd urine type smell. The only flowers that really stuck out in my mind as beautiful were the ones sent by my mother’s former employers from when we lived in California.

As an early warning, when I do die, people are welcome to leave letters on my grave and tuck them in the earth. I will greatly appreciate it if people donate their money to a charity instead of spending that money on flowers. After two deployments, I can also say I don’t want my family to waste my life insurance money on remembering me. It’s money for them to maintain their dreams and to keep their basic needs met so they are not burdened unnecessarily whenever it is my time to go.